Financing options significantly impact the overall cost of solar panels primarily through differences in upfront payments, interest rates, loan terms, and ownership benefits. Here’s a detailed breakdown of how various financing methods affect the total cost:

Financing Methods and Their Impact on Cost

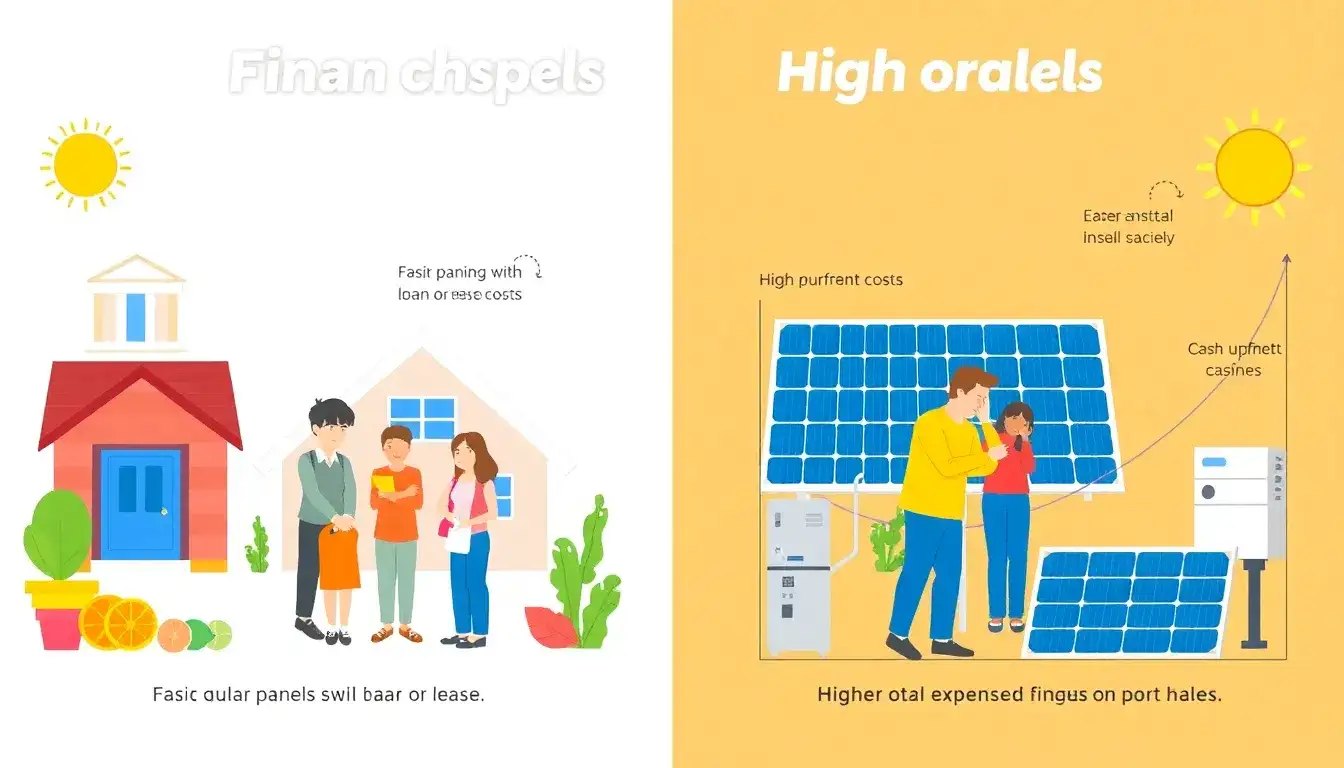

1. Cash Purchase

– Paying cash upfront is the cheapest way to finance solar panels because it avoids any interest or loan fees.

– With cash purchase, you own the system outright immediately, allowing you to fully benefit from tax incentives like the 30% federal investment tax credit (ITC) and other rebates, accelerating your return on investment.

– Since there are no loan repayments, your monthly electricity savings begin right away without being offset by financing costs.

– The downside is the high initial capital requirement, typically $20,000 to $30,000 or more before installation.

2. Solar Loans (Personal Loans, Home Equity Loans, Contractor Financing)

– Solar loans allow you to spread out the cost over time, usually 5 to 25 years, with fixed monthly payments and interest.

– Loans like personal loans are often unsecured but require good credit for the best rates; home equity loans usually offer lower interest rates and tax-deductible interest but use your home as collateral.

– Contractor financing is convenient and may offer competitive rates but can include origination fees and longer loan terms, which increase total interest paid.

– Despite interest costs, solar loans often still offer financial sense since you own the system and can claim tax incentives, though total cost ends up higher than cash purchase due to interest.

3. Solar Leases and Power Purchase Agreements (PPAs)

– These options typically require little to no upfront payment but do not convey ownership of the solar system.

– You pay a fixed monthly lease fee or pay per kilowatt-hour generated, which can add up to amounts potentially comparable to or exceeding the cost of buying solar outright over time.

– Because you don’t own the system, you are often ineligible for tax credits and rebates.

– Maintenance and repairs are handled by the leasing company, reducing your responsibility but also reducing long-term savings.

– These options may suit those with limited upfront funds or who do not want to maintain the system but generally result in higher overall costs and lower return on investment.

Additional Factors That Affect Overall Cost

- Interest and Fees: Financing options with longer terms or higher interest rates increase the total amount paid. Origination or dealer fees with some contractor loans or credit union loans also add to costs.

- Tax Incentives: Ownership (via cash or loans) enables you to claim the federal ITC and other state/local incentives which substantially offset costs. Leases and PPAs typically do not allow tax credit benefits to the homeowner.

- Home Value: Owning solar panels can increase your home’s resale value by about 6.8% on average, an added financial benefit sensitive to location and system size.

- Loan Terms: Longer loan terms reduce monthly payments but increase total interest paid over time, potentially offsetting immediate cash flow benefits.

- Convenience vs. Cost Trade-off: Financing through contractors is convenient but may lock you into longer terms or fees. Personal and home equity loans may offer better rates but require more effort to secure.

Summary Table: Financing Impact on Solar Panel Cost

| Financing Option | Upfront Cost | Ownership | Interest/Fees | Tax Incentives Eligibility | Total Cost Impact | Typical Use Case |

|---|---|---|---|---|---|---|

| Cash Purchase | High | Yes | None | Yes | Lowest total cost, highest upfront | Best for those with available capital |

| Solar Loan (Personal, Home Equity, Contractor) | Low to Moderate | Yes | Interest + possible fees | Yes | Moderate overall cost due to interest | Those wanting ownership but lacking cash |

| Solar Lease / PPA | Very low or none | No | Monthly fees, no interest | No | Higher long-term cost, no ownership | Low upfront cost, no maintenance, no ownership |

In conclusion, financing choices influence not only the immediate affordability of solar panels but also their long-term cost-effectiveness. Paying cash or using low-interest loans generally results in the lowest overall cost due to ownership benefits and tax credits, while leasing or PPAs reduce upfront costs but increase total expenditure and reduce financial returns.

Original article by NenPower, If reposted, please credit the source: https://nenpower.com/blog/how-do-financing-options-impact-the-overall-cost-of-solar-panels/